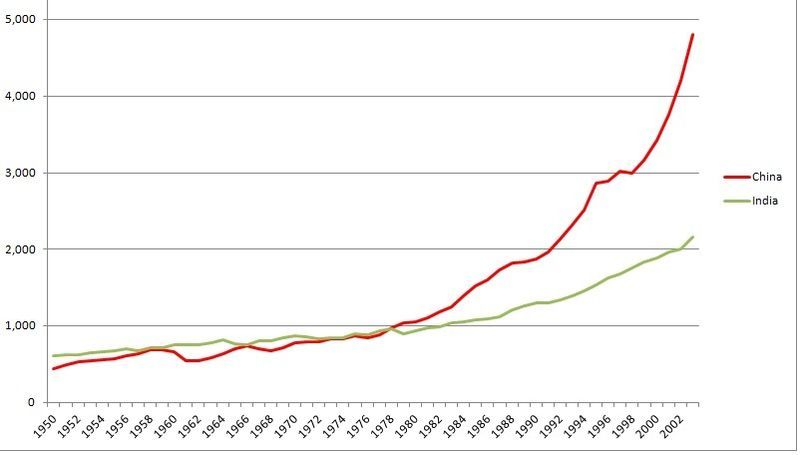

Lets have a look at something more recent and relevant:

http://www.imf.org/en/News/Articles...strong-growth-persists-despite-new-challenges

For India, Strong Growth Persists Despite New Challenges

February 22, 2017

- India remains one of the fastest growing emerging market economies

- Due to recent cash shortages, growth is projected to slow temporarily this fiscal year

- Maintaining the reform momentum is key to stronger growth

India’s overall outlook remains positive, although growth will slow temporarily as a result of disruptions to consumption and business activity from the recent withdrawal of high-denomination banknotes from circulation.

But the nation's expansion will pick up again as economic reforms kick in, said the IMF in its latest assessment. Growth is expected at 6.6 percent in this fiscal year and at 7.2 percent in the following year.

Speaking to

IMF News, IMF mission chief for India Paul Cashin discusses these and other challenges, and also highlights the opportunities for this vibrant economy moving forward.

IMF News: The IMF just completed its annual assessment of the Indian economy. How is the economy doing?

The Indian economy is growing strongly and remains a bright spot in the global landscape. The halving of global oil prices that began in late 2014 boosted economic activity in India, further improved the external current account and fiscal positions, and helped lower inflation. In addition, continued fiscal consolidation, by reducing government deficits and debt accumulation, and an anti-inflationary monetary policy stance have helped cement macroeconomic stability.

The government has made significant progress on important economic reforms, which will support strong and sustainable growth going forward. In particular, the upcoming implementation of the goods and services tax, which has been in the making for over a decade, will help raise India’s medium-term growth to above 8 percent, as it will enhance the efficiency of production and movement of goods and services across Indian states.

Challenges remain, however, and there is little scope for complacency. A key concern for us is the health of the banking system, which is still dealing with a large amount of bad loans, and also heightened corporate vulnerabilities in several key sectors of the economy.

And, over the past few months, the economy has been hit by cash shortages, and accordingly we reduced our growth forecasts to 6.6 percent for fiscal year 2016/17 and to 7.2 percent in 2017/18.

IMF News: How is this recent “demonetization” initiative affecting the economy, and what are some of the long-term ramifications?

The initiative affected notes with a total value of about 15 trillion rupees, which amounted to 86 percent of all cash in circulation. Because payment transactions in India are primarily cash-based and electronic payments infrastructure is limited, the shortage of cash has disrupted economic activity, with smaller businesses and rural regions being particularly badly affected.

Fortunately, these effects are expected to gradually dissipate by March 2017 as cash shortages ease. It also appears that measures taken to alleviate payment disruptions, such as temporarily allowing use of old banknotes for purchases of fuel and agricultural inputs, have helped mitigate the negative impact. So we expect the slowdown to be limited and relatively short-lived and the financial system to come through unscathed. Of course, potential loan repayment risks should be monitored carefully, particularly given an already elevated level of non-performing loans.

The demonetization initiative presents an opportunity to increase the size of the formal economy and broaden financial intermediation in the longer term. It can also support a widening of the tax base, help reduce the fiscal deficit, enhance bank liquidity, and give a fillip to the government’s efforts to promote greater financial inclusion.

IMF News: How can India ensure that the fruits of its growth are shared by all?

India has made appreciable progress on several fronts. It achieved its

Millennium Development Goals of halving poverty, infant and child mortality, and maternal mortality rates. Students are now staying in school longer, as evidenced by an increase in secondary school completion rates. Moreover, significant progress has been made in enhancing financial inclusion, leveraging technology to bring more of the population into the financial system.

However, progress on improving health, nutrition, and sanitation has been less encouraging, income inequality has risen, and employment growth has been sluggish. For instance, a very large share of Indian workers—more than 90 percent—remain employed in low-productivity informal sector jobs. Women’s participation in the labor force is also low at around 25 percent—the lowest among emerging markets. Further labor market reforms, at both the center and state levels, are needed to encourage better quality job creation and raise female labor force participation.

While there has been important progress, we see scope to pursue better targeting and greater efficiency of subsidy and social spending programs through greater use of the trio of

Aadhaar unique beneficiary identification, direct benefit transfers, and information technology. Finally, more needs to be done to raise agricultural productivity and enhance market efficiency. This would help increase supply of high-value foods, enhance returns to farmers, and dampen food inflation pressures.

IMF News: As India’s economy becomes increasingly sophisticated, how does the government keep pace with its capacity to craft sound economic policy?

Sound economic policymaking underpinned by strong institutions is critical for sustainable growth. A recent example of a positive change in India is the implementation of flexible inflation targeting and creation of the Monetary Policy Committee, which have strengthened the credibility of monetary policy and helped maintain price stability in an increasingly complex economy.

In addition to providing policy advice, the Fund is committed to working with the Indian authorities to help build capacity for policymaking. The recently inaugurated

South Asia Regional Training and Technical Assistance Center(SARTTAC) headquartered in New Delhi—which will serve Bangladesh, Bhutan, India, Maldives, Nepal, and Sri Lanka—is the first IMF-supported center to combine both technical assistance and training.

The center will provide training to government and public sector employees, enhance their skills and improve the quality of their policy inputs, and will also provide technical assistance to governments and public institutions. SARTTAC is expected to become the focal point for planning, coordinating, and implementing the IMF’s capacity development activities in the region on a wide range of areas, including macroeconomic and fiscal management, monetary operations, financial sector regulation and supervision, and macroeconomic statistics.

Full paper (worth looking at):

http://www.imf.org/en/Publications/...f-Report-and-Statement-by-the-Executive-44670