Optimizing the Eurozone by Koichi Hamada - Project Syndicate

BUSINESS & FINANCE

KOICHI HAMADA

BUSINESS & FINANCE

KOICHI HAMADA

Koichi Hamada, Special Economic Adviser to Japanese Prime Minister Shinzo Abe, is Professor of Economics at Yale University and Professor Emeritus of Economics at the University of Tokyo.

OCT 28, 2014

Optimizing the Eurozone

TOKYO – The eurozone is facing a bleak economic outlook, with growth remaining stagnant and the threat of deflation looming large. The economist

Martin Feldstein, who was skeptical of the initiative from the start, now calls it a “failure.” Is Feldstein right, or could the eurozone become the “optimal currency area” that its creators believed it to be?

Answering this question requires, first and foremost, an understanding of the costs and benefits of various exchange-rate systems. The International Monetary Fund was established 70 years ago to manage an “adjustable peg” system – a hybrid system in which exchange rates were usually fixed to the US dollar, but could be adjusted occasionally to improve the country’s competitive position in export markets.

For the first few decades, this system leaned heavily toward “peg,” owing to the US dollar’s direct convertibility to gold. This brought significant stability to the global monetary order, following the competitive devaluations of the 1930s that some economists considered damaging.

But the fixed exchange-rate system also undermined the United States’ capacity to manage its balance of payments. That is why, in 1971, President Richard Nixon unilaterally abandoned the dollar’s convertibility to gold, leaving major currencies’ exchange rates to float against one another.

Such a system provides important advantages – most notably, it enables the US Federal Reserve to pump money into the economy to prevent or halt a recession. But it also carries serious risks, exemplified in the trade imbalances that emerged in the 1980s.

From 1980 to 1985, the US dollar appreciated by 50% against the currencies of Japan, West Germany, France, and the United Kingdom; America’s current-account deficit was approaching 3% of GDP; and its top four competitors had massive surpluses and negative GDP growth. In order to correct these imbalances, the five countries signed the

Plaza Accord, in which they agreed to intervene in currency markets to devalue the dollar.

It is against this background that the euro was born, with the goal of boosting European economies by expanding their “local” market, lowering transaction costs, and facilitating the flow of information. In 1991, the loss of monetary-policy independence seemed like a worthwhile trade-off for Europe’s economies; today, it seems that it may have been a mistake.

In fact, America’s experience in the 1960s should have warned the eurozone’s creators that tying national monetary authorities’ hands might not be such a good idea. That would not be the case if the eurozone operated according to

Robert Mundell’s vision of an optimal currency area, with labor and capital adjustments replacing exchange-rate adjustment, and shocks being homogeneous (rather than asymmetric). Moreover, Germany’s experience with reunification suggests that political union is integral to such a union’s success.

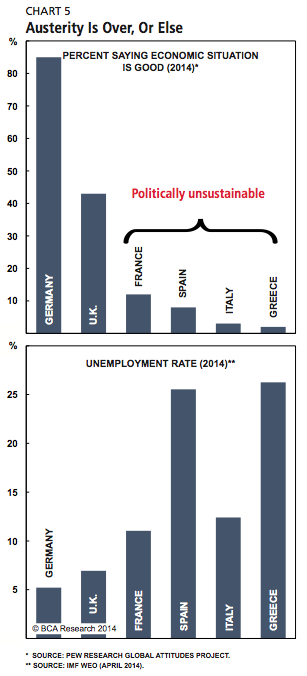

The eurozone’s performance has not met any of these criteria. Most notably, eurozone countries have faced powerful asymmetric shocks, to which their lack of independent monetary-policy instruments made it virtually impossible to respond. As a result, they have struggled with recurring economic crisis.

To understand the corrective power of monetary policy, one need only consider Japan’s recent progress in escaping from decades of stagflation. Monetary expansion was one of the three key features of Prime Minister Shinzo Abe’s economic strategy – an approach that could have been implemented years ago to halt the yen’s sharp appreciation. The problem was that Bank of Japan Governor Haruhiko Kuroda’s predecessors behaved as if they were bound by a fixed exchange-rate regime.

Unlike in Japan, eurozone countries’ failure to implement bold monetary-policy measures is not a choice. The only available monetary-policy tool is to change collectively the euro’s value relative to outside currencies. But use of this tool is constrained by the wide discrepancies among individual countries’ appetite for inflationary or deflationary price levels.

To be sure, European economic integration – a process that, one might say, culminated with the eurozone’s establishment – also brought clear political benefits. As Robert Schuman promised when he conceived the idea of a European Community, integration has prevented the recurrence of war between Germany and France. But whether monetary union on such a large scale was necessary to achieve this goal is dubious.

In any case, the eurozone exists – and, at this point, it would be exceedingly difficult to dismantle it fully. Given this, the goal today should be to move toward an optimal currency area.

For starters, Europe’s leaders must recognize that the eurozone, as it is currently constituted, is larger than Europe’s optimal currency area. Some of its member countries – certainly Greece, and probably Italy and Spain – need an independent monetary policy. Otherwise, they will continue to go from one crisis to the next, with countries that do fall within the optimal currency area – for example, Germany and France – facing the consequences.

Once membership in the eurozone is optimized, the next step will be to ensure continued progress toward political consolidation. The result will be a stronger, more efficient eurozone – one in which the benefits really do outweigh the costs.

Optimizing the Eurozone by Koichi Hamada - Project Syndicate

Read more at

Optimizing the Eurozone by Koichi Hamada - Project Syndicate

This is not Soviet Russia were discontent with the party line is forbidden.Suck it up comrade Trollintski

This is not Soviet Russia were discontent with the party line is forbidden.Suck it up comrade Trollintski

")