Turkey heads for record current account surplus

Turkey may have notched up the largest monthly current account surpluses in its history in August and September, as a painful currency crisis appears to have led to a rapid rebalancing of the country’s economy.

The Turkish lira has plummeted 38.4 per cent against the dollar this year as foreign investors have been scared off by president Recep Tayyip Erdogan’s well-publicised opposition to the interest rate rises that most economists deem necessary to rein in an overheating economy.

Preliminary data released this week by the trade ministry suggested the goods trade deficit fell to $1.9bn in September, a 77 per cent decline from the same month last year. This follows similar year-on-year declines of 59 per cent in August and 33 per cent in July, as the first chart shows.

Importantly, though, for the health of Turkey’s economy, there are signs that the adjustment is not just happening because consumers and businesses are cutting back on imports due to rising prices.

While imports fell 18 per cent year-on-year in September (and 23 per cent in August), exports jumped 23 per cent to a record September tally of $14.5bn, as depicted in the second chart. This took Turkey’s export-import coverage ratio to 88.4 per cent, from 59.1 per cent 12 months earlier.

“There has only been one month since 2012 when exports have been stronger than what the preliminary data are showing us,” said Charles Robertson, chief economist at Renaissance Capital, an investment bank. That was in July 2017, when exports rose 28 per cent. “It’s curious.” “The correction seems to be quicker and stronger than many expected,” said Nora Neuteboom, economist at ABN Amro. D

Data from the Turkish Exporters Assembly suggest September’s surge in exports was broad-based, with all major sectors participating. Automotive exports rose 21 per cent year-on-year to $2.6bn, agricultural produce 16.5 per cent to $1.9bn, apparel 13.8 per cent to $1.5bn and steel exports an impressive 95 per cent to $1.4bn.

The figures are merely the latest to point to a rapid restructuring of the economy. Car sales plunged 67 per cent year-on-year to 17,595 units in September while the manufacturing purchasing managers’ index slid to a near-decade low of 42.7, consistent with a recession — even before a sweeping austerity programme kicks in to tackle a jump in consumer price inflation to 24.5 per cent and a surge in producer price inflation to 46.2 per cent.

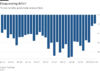

Moreover, Mr Robertson estimated that Turkey would record a current account surplus of $2.1bn in each of August and September, far higher than for any month since his records began in 1992, as the final chart indicates, and the first surplus of any description since a tiny one in August-September 2015. These forecasts are based on factoring in Turkey’s traditional surplus in services, particularly noticeable in summer months when tourism is in full swing, and remittance flows, on top of the goods trade data.

“The trade deficit is improving in the months where there is a lot of tourism and there has been more tourists this year than ever,” Mr Robertson said. While he does not expect that Turkey will continue to produce monthly current account surpluses as winter approaches, Mr Robertson said the rolling 12-month deficit, which peaked at $58bn in May, was likely to fall to about $6bn by July 2019.

A marked rebound in Turkish exports, if maintained, could have ramifications on the global stage. While a rise in exports in the wake of a sharp currency depreciation is entirely consistent with economic theory, it appears to be rather more elusive in practice.

Gita Gopinath, the new chief economist of the IMF, has argued that gains from flexible exchange rates “are less than you think”. In a 2015 paper, Ms Gopinath, then a Harvard University professor, wrote that “an exchange rate depreciation is perceived to make a country’s exports immediately cheaper on world markets. However, for the vast majority of countries whose exports are invoiced in a foreign currency [such as Turkey] this is unlikely to be the case.” As a result, in such countries a currency depreciation does little to increase the volume of exports but does increase the profits of exporters.

This contrasts with situation in the US, where 97 per cent of exports are invoiced in local currency. Ms Gopinath consequently concluded that: “trade balance adjustments, through relative price effects, are more likely to be driven by adjustments in exports in countries like the US, while being driven by adjustments in imports in countries like Turkey.”

The IMF itself concluded in the same year that weaker exchange rates have not lost their power to spur higher exports, citing research that found that a 10 per cent real effective depreciation of a currency raised real net exports (ie exports minus imports) by, on average, 1.5 per cent of GDP, with about half of this effect stemming from a rise in exports and half from a fall in imports.

Ms Gopinath’s conclusions do, though, support research by the World Bank, which found that currency devaluations are now only half as effective at boosting exports as they were in the mid-1990s. Her findings are also in line with analysis by the FT in 2015, focused purely on emerging markets, which found that during the two previous years currency weakness had not boosted exports at all, although it had led to a drop in imports.

As to whether or not Turkey has definitively bucked the trend will depend on further data. For now, Ms Neuteboom admitted to being “a bit puzzled” by the data, especially because Turkey has a large import component in its exports.

“Usually, countries that possess a lot of natural resources and are a net commodity exporter see these huge current account deficit corrections taking place, [but] Turkey is not a net commodity exporter,” she said. Ms Neuteboom did point out, though, that some of Turkey’s major export markets, such as Germany and the US, are growing strongly, which “should support a recovery, but perhaps not as swift as we are seeing now”.

One other factor behind September’s export surge could be that exports in August were weak, falling 6.5 per cent year-on-year to $12.4bn. Mr Robertson attributed this to a working-day effect, with four fewer working days this August than in August 2017 because of religious holidays. This could mean some of August’s activity was shifted to September, although even if that is so, average export growth over the past three months will still have been strong. “At the moment it’s looking like it’s going to be a really impressive recovery and mean that only one emerging market [in the MSCI equity index], Pakistan, has a current account deficit of 3 per cent [or more],” Mr Robertson added.

https://www.ft.com/content/e5924bc0-c71f-11e8-ba8f-ee390057b8c9